One Less Thing to Worry About When Opening Your Practice

The thought of opening your own practice is thrilling – the prospect of being your own boss and building something all your own is no doubt one of the most exciting endeavors in any profession. However, it can be a little scary too, knowing you’re entirely responsible for every aspect of your livelihood. Ensuring you’ve filed all the proper forms and secured adequate office space can be daunting enough, but there are a lot of other details that can add stress and confusion to this exciting time.

To alleviate at least one of these, we’ve assembled a quick guide to help you better understand lawyers professional liability (LPL) insurance – a vital piece of protection you and your firm will need.

THE BASICS

Insurance is a risk management strategy that can bring much-needed peace of mind. The unfortunate truth is even the most diligent lawyers can be sued. In fact, the ABA says attorneys in private practice should expect two to three claims during their careers. Claims – even those without merit – are not only time-consuming but can be expensive to defend. Plus, in the event an error or omission is found, it can take tremendous resources to make a client whole.

To help our insureds rest even easier, OAMIC LPL policies include a claims expense allowance, which is applicable to defense costs only and is provided in addition to the per claim limit (except in the case of a securities-related claim).

WHAT KIND OF POLICY DO YOU NEED?

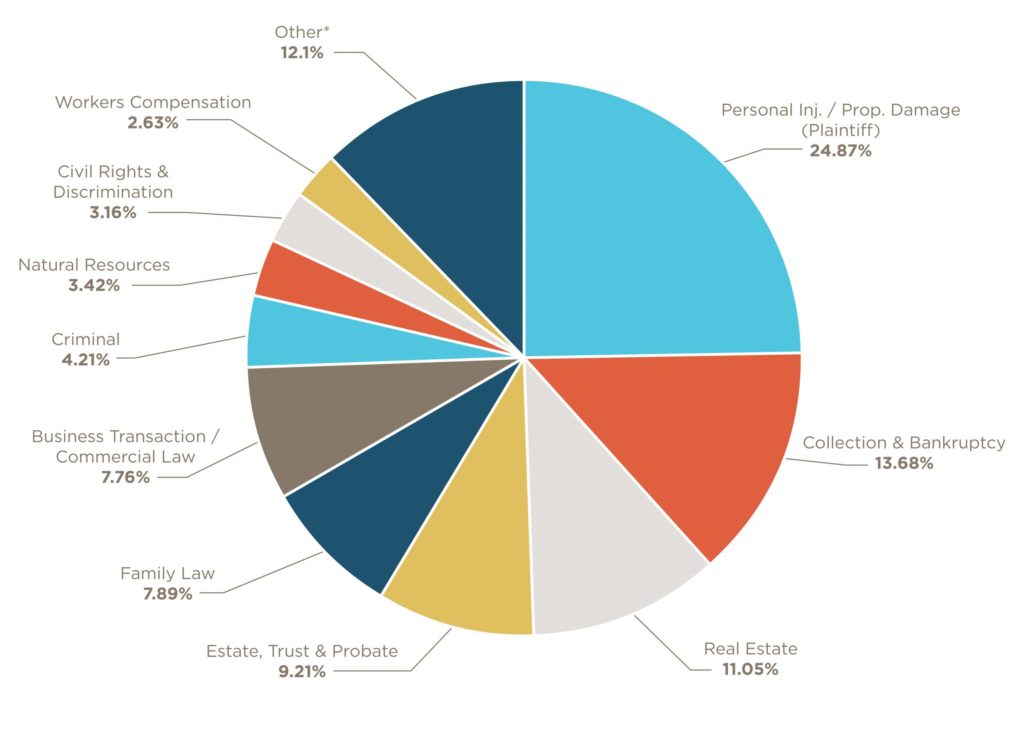

Most people are surprised to learn that the terms “professional liability,” “errors and omissions (E&O),” “malpractice” and even “professional indemnity” are all names for essentially the same thing. There are some superficial differences – such as, although “malpractice insurance” is technically a type of insurance for those in the medical profession, it has been adopted as a colloquial term for liability insurance in most professions – but they all generally describe the coverage which includes acts or omissions for legal services rendered by the firm.

UNDERSTANDING LIMITS

LPL limits are listed as a smaller number over a larger number, like 200/600. The first number indicates the maximum per-claim limit and the second number is the aggregate for the policy year (in this example, $200,000 per claim and $600,000 for the policy year).

When deciding how much coverage you need, carefully consider the value of matters you handle and plan accordingly. As OAMIC’s president, Phil Fraim, says, “Unfortunately, there’s no magical formula to determine the appropriate limit – unless, of course, you can tell me what you are going to be sued for.”

- Read more: What Do Split Limits Mean? and If LPL Is Important, Are Limits Also?

WHO LPL COVERS

Now that you’ve considered what to cover, it’s time to look at who you’re covering.

Your policy is issued to the law firm as a whole, and not individually to each attorney. Every licensed attorney who is associated/affiliated with the firm will be listed as a named insured. This is primarily due to the potential vicarious liability or partnership by estoppel created from the existence of a firm.

All non-lawyer employees are also covered for work related to legal services provided (unless they are listed in the policy exclusion list). There is no premium charged for those not specifically named, as their work is viewed as assistance to the legal work provided by the attorneys in the firm and are ultimately their responsibility.

WHY IS CONTINUITY IMPORTANT?

Professional liability insurance is written as a claims-made policy. In order for an incident to be covered under a claims-made policy, two things must be true. First, you need to have insurance when the claim is made. Secondly, you need to have a policy in place when the incident occurred. The insurance policy in effect when the claim is made is the one that actually responds to the claim, hence the name claims-made. So, if an error occurred in 2018 but isn’t reported until 2021, you need to have had coverage from 2018 to 2021. This is why continuity of insurance is important. Each year you renew your policy, it will cover you for the year ahead, as well as back to the start date of the first claims-made policy you purchased.

LPL is structured this way because of the length of time that can occur between the work being done and the claim being made. In the state of Oklahoma, the related statute of limitations is based on discovery of the error, which can sometimes be a decade or more.

OTHER PROTECTION YOU MAY NEED

Although LPL insurance is by far one of the most important forms of risk management for your firm, you may have other needs with respect to protection. Office package policies can protect assets like furniture, equipment, valuable papers, loss of income and employee dishonesty. Cyber liability coverage is included with every LPL policy OAMIC issues – including legal forensic, public relations, cyber extortion and regulatory defense penalties – but limits can also be increased to provide even more protection against cyber threats.

If you have employees, you are also required by Oklahoma law to carry workers compensation insurance to protect your business and employees from hardships of workplace accidents. Also related to employees is employment practices liability coverage, which protects against claims made by employees alleging discrimination, wrongful termination, harassment and more.

- Read more: Additional Products

WORRY ABOUT ONE LESS DETAIL

We want all Oklahoma law firms to be successful, and as Oklahoma attorneys’ local provider of LPL, we’re here to support you. Whether you have questions about your policy or just want information about our products, you can always contact our staff directly by phone or email. Because we know you’re busy, especially when running your own practice, we use a short, four-page application for new or renewal applications, which allows us to return your quote within 24 hours.

For less cost than you may think, you can get coverage that lets you focus on what’s most important to you: your practice and how to best serve your clients. With everything to worry about when it comes to opening and running your firm, don’t let the risk of claims be one of them. As always, contact us if we can help you learn more or if you have specific questions about options.